Why Solo Law Firms Stay Busy but Fail to Build Real Wealth

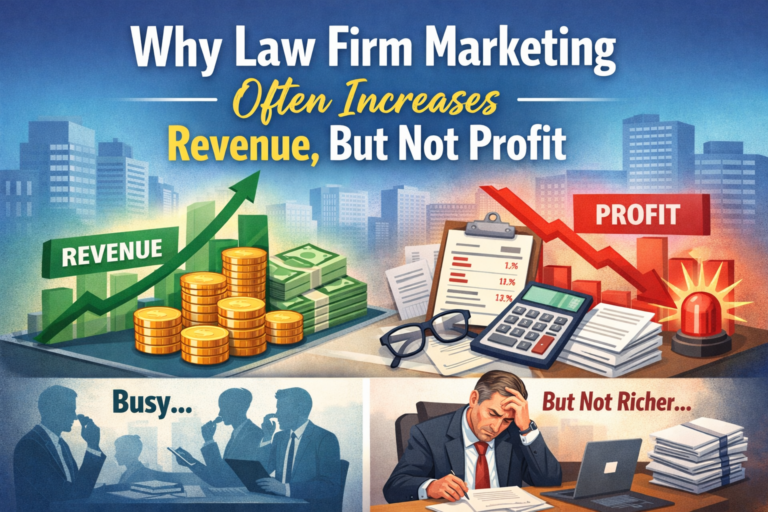

Many solo lawyers are busy but stay broke. While a full calendar and ringing phone look like success, there is often very little money left for you after paying rent, staff, and software. This gap between working hard and actually keeping money is the biggest barrier to building wealth.

The real problem is that being busy doesn’t always mean you are making money. You can work 60 hours a week, but if you only bill 15 of them, your business isn’t healthy. To turn a stressful job into a business that builds your future, you must find where your money is leaking and fix the system.

The Real Problem: Money Breaks Down at Every Stage

Financial success in a law firm follows a linear flow. When this flow is interrupted, wealth never materializes.

Time – Revenue – Cash – Profit – Wealth

Most solo firms don’t have a “top of the funnel” problem; they have enough work. They have a leakage problem. They lose value between these steps, often failing to convert their grueling hours into actual bank balance growth.

The 4 Financial Breakdowns That Keep Law Firms Stuck

1. The Utilization Gap: Why Your Calendar is Full but Your Bank Account Isn’t

The first major leak in a solo practice is the vast chasm between “working hours” and “billable hours.” While most lawyers feel the exhaustion of a 50-hour work week, the uncomfortable reality is that actual billable output often hovers between only 10 and 15 hours. The remainder of that time is silently swallowed by administrative drift, including unbilled client check-ins, initial intake conversations, and the constant friction of chasing paperwork. This creates a misleading sense of productivity that feels like progress but never actually translates to the bottom line.

This discrepancy leads directly into pricing pitfalls because many solo practitioners set their rates based on market pressure or a vague sense of what feels “fair” compared to the firm down the street. If your pricing model assumes a 40-hour billable week but you are only actually billing 15, your effective hourly rate is a mere fraction of what you intend, leaving you underfunded for the actual labor performed. To fix this, your pricing structure must be rebuilt from the ground up to cover not just your active time, but also your overhead, taxes, and a mandatory profit margin that accounts for those non-billable administrative hours.

2. The Cash Flow Trap: Moving From Revenue to Realized Capital

It is a hard truth in business that revenue is a vanity metric while cash flow is the only measure of sanity. You can technically be profitable on paper and still face a crisis because you lack the liquid cash to pay your assistant or your rent on Friday. Many lawyers fall into the “lender trap” by performing work without an upfront retainer, which effectively turns the law firm into a 0% interest lending institution for the clients. This places all the financial risk on the attorney’s shoulders rather than the consumer of the legal services.

The solution is to implement strict retainer-first policies where the work simply does not commence until the trust account is properly funded. By shifting to a model where you are paid before the labor is expended, you eliminate the need to chase collections and drastically reduce your operational risk. Furthermore, maintaining a dedicated cash reserve of 3 to 6 months of operating expenses is essential to killing the “feast or famine” cycle that plagues most small firms, providing a buffer that allows for strategic decision making rather than decisions made out of financial desperation.

3. Margin Erosion: Defending Your Profit Against Hidden Costs

Even when a firm has consistent cash flow, hidden costs can erode profit margins before the owner can take a draw. Small expenses like software subscriptions, bar dues, continuing education, and professional liability insurance can quietly compound, eating away at your take-home pay without being noticed. Without a granular understanding of these outflows, a lawyer cannot distinguish between a necessary investment that grows the firm and a wasteful expense that merely reduces their personal wealth.

Beyond simple profitability, there is a significant compliance risk associated with poor financial tracking. Without accurate, professional bookkeeping, you risk more than just low profits; you risk your license to practice law. Mishandling IOLTA accounts or commingling funds due to sloppy record-keeping is the fastest route to a serious ethical violation and an appearance before the bar. Professional systems and regular financial reviews are not optional luxuries, they are foundational requirements for protecting both your professional career and your personal capital.

4. The Wealth Engine: Transitioning From a Job to a Scalable Business

The final hurdle to building wealth is the lack of a system to actually retain and grow the money the firm generates. Many solo practitioners treat their business account like a personal piggy bank, withdrawing whatever happens to be left over at the end of the month without a long-term plan. This lack of structure leads to the inevitable “tax surprise,” where April becomes a period of deep financial stress because quarterly obligations were never factored into the monthly budget or set aside in a dedicated account.

Furthermore, if the firm’s ability to generate income is entirely dependent on you sitting at your desk every day, you do not actually own a business; you own a high-stress, high-liability job. To transition into a wealth-building entity, you need a financial team consisting of a bookkeeper for records, a CPA for tax compliance, and a fractional CFO or advisor for long-term strategy. This team ensures you are paid a consistent salary and that the firm’s surplus is being redirected into investments and systems that grow independently of your daily billable labor.

What Financially Strong Law Firms Do Differently

Financially successful firms stop guessing and start tracking their Realization Rate, which is the gap between the hours they work and the actual cash they collect. They realize that “busy” is a trap, so they price their services to cover not just their legal work, but also the unbilled hours spent on administration, taxes, and overhead. This ensures that every hour worked contributes to the firm’s actual profit, not just its activity.

To stay efficient, these firms use practice management software to automate billing and collections, making it effortless for clients to pay immediately. Most importantly, they turn their daily tasks into Standard Operating Procedures (SOPs). By documenting exactly how to handle intake or filing, they can delegate routine work to a $25-per-hour assistant. This shift allows the lawyer to stop acting as a high-paid clerk and start acting as a CEO who focuses on high-value strategy and long-term wealth.

Practical Framework: Turning Activity Into Wealth

- Audit Your Numbers: Calculate your total expenses and divide them by your actual billable hours. Is your rate high enough?

- Fix Cash Flow: Shift to evergreen retainers or flat fees paid upfront.

- Build Your Reserve: Set aside 10% of every payment until you have 3 months of “runway.”

- Hire a Pro: Move beyond “DIY” accounting. A professional bookkeeper pays for themselves in found time and tax savings.

- Standardize: Create a checklist for every recurring task (intake, filing, closing a file).

Busy Is Not the Goal—Wealth Is

Success in law isn’t measured by the thickness of your case files or the hours on your timesheet. It is measured by the stability and freedom your firm provides you. Without financial clarity and rigorous systems, a busy law firm is just a demanding boss that you can never quit.

True wealth is built when the business serves the owner, rather than the owner serving the business.

Read More: The Biggest Mistake Law Firms Make When Scaling Their Marketing

Self-Made CFO is an independent financial insights platform focused on CFO-level thinking for businesses operating in complex, regulation-driven industries, particularly law firms and med spa businesses.

The platform curates analysis, frameworks, and perspectives designed to help founders and operators better understand financial decision-making beyond day-to-day accounting.